The 50/30/20 Rule: How to Budget Your Money in 3 Simple Steps

Life is tough enough without trying to keep up with an overly complicated budget. About 58% of Americans live paycheck to paycheck, according to The Penny Hoarder’s State of Savings survey — meaning savings, not just spending, is where most household budgets break down. When the numbers feel that overwhelming, a complicated budgeting system is usually the first thing to go.

But forgoing budgeting altogether isn’t the answer — in fact, it can compound the problem. According to the The Penny Hoarder’s Financial Anxiety Barometer report, 65% of Americans say essential living expenses are their biggest source of financial anxiety. Knowing that you have the basics covered can help alleviate some of the stress, and using a simple budget can help ensure you stick with it.

That’s why so many people start with the 50/30/20 rule. It splits your after-tax income into three simple buckets — needs, wants and savings — without forcing you to track every coffee or grocery run. The framework was popularized by Senator Elizabeth Warren in her book All Your Worth: The Ultimate Lifetime Money Plan, and it remains one of the most beginner-friendly budgeting methods because the math is fast and the categories are forgiving.

How much should actually go to needs vs. wants? What if your rent already eats more than half your paycheck? And which apps make this kind of budgeting easier? We’ll answer all of these questions and more below.

Quick Comparison: Best Budgeting Apps of 2026

Here’s a quick look at our roundup of the best budgeting apps.

| Budgeting App | Price | Best For | Free Version |

|---|---|---|---|

| Rocket Money | Free; $7–$14/mo for Premium | Subscription tracking, all-in-one | Yes |

| Monarch Money | $14.99/mo; $99.99/yr for Core plan | Couples and full-picture tracking | No (7-day trial) |

| Piere | Free; $29.99/year for Piere Platinum | Set-and-forget savings | Yes |

| YNAB | $14.99/mo or $109/yr | Zero-based budgeting | No (34-day trial) |

| Cleo | Free; $5.99/mo for Plus | Fun, AI-chatbot engagement | Yes |

| Quicken Simplifi | $6.99.mo, billed annually | Beginners, light users | No (30-day money-back) |

| EveryDollar | Free; $17.99/mo or $79.99/yr for premium | Dave Ramsey followers, Baby Steps users | Yes (requires manual entry) |

| PocketGuard | $12.99/mo for Plus | Knowing what's safe to spend | Yes, but difficult to access |

What Is the 50/30/20 Rule?

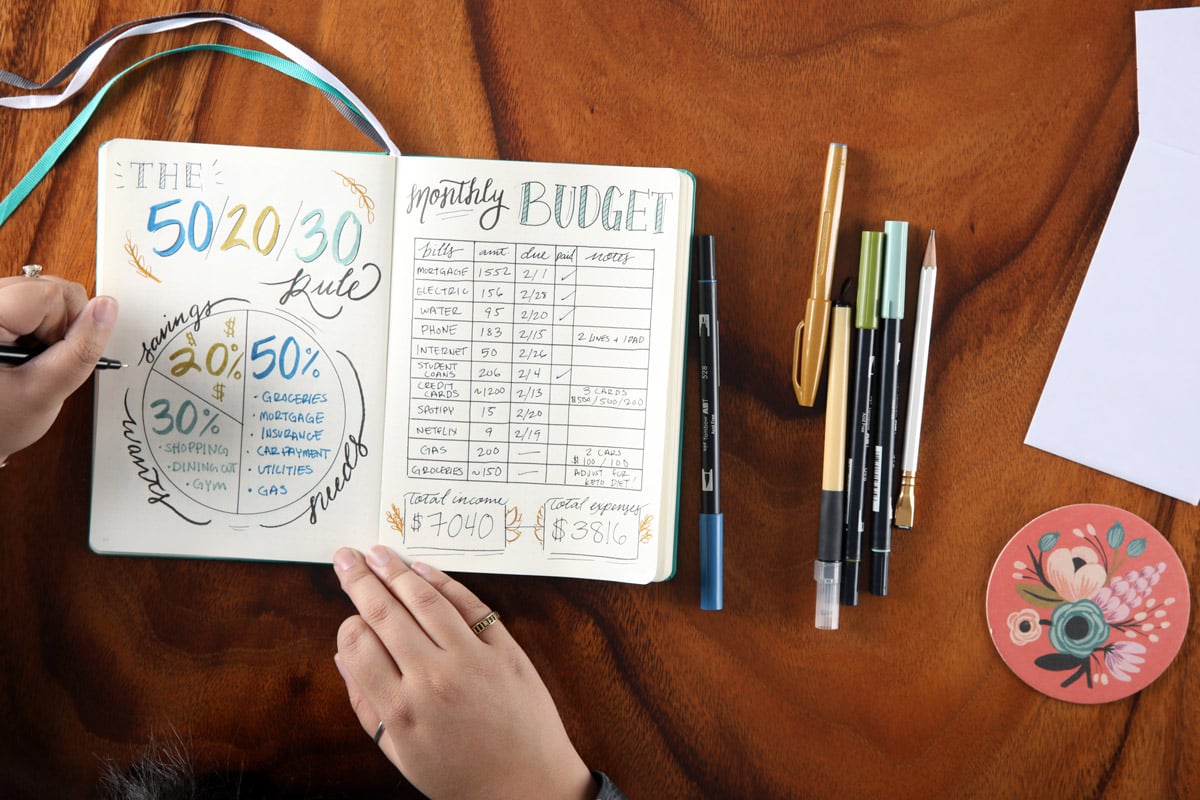

The 50/30/20 rule is a budgeting guideline that divides your after-tax income into three categories: 50% for needs, 30% for wants, and 20% for savings and debt repayment — making it one of the simplest frameworks for anyone starting a budget.

The key word is after-tax. The rule uses your take-home pay — the amount that actually lands in your bank account on payday — not your gross salary. Using gross income is one of the most common beginner mistakes and can throw the entire budget off.The framework was introduced by Elizabeth Warren and her daughter Amelia Warren Tyagi in All Your Worth, where they argued that most people don’t need detailed category-by-category tracking — they just need a clear ceiling for needs and wants and a floor for savings.

What Counts as Needs, Wants and Savings?

Needs are expenses you can’t avoid — rent, utilities, groceries, insurance, minimum debt payments — while wants are optional spending that improves your quality of life, like streaming subscriptions, dining out or gym memberships. Savings includes anything you set aside for the future, including extra debt payments above the minimum.

| Needs (50%) | Wants (30%) | Savings/Debt (20%) |

| – Rent or mortgage – Utilities (electric, water, gas) Groceries – Insurance (health, auto, renters) – Minimum debt payments – Transportation (car payment, transit) |

– Dining out and takeout – Streaming services – Gym memberships – Hobbies and entertainment – Travel and vacations – Shopping beyond necessities |

– Emergency fund – Retirement contributions (401(k), IRA) – Extra payments toward high-interest debt – Savings goals (vacation, car, home) – Investing (brokerage, index funds) – Sinking funds for irregular expenses |

Some line items live in a gray area. A gym membership might be a want for one person and a mental-health need for another. The trick is to be consistent — pick a category and stick with it month to month so your numbers stay comparable. For a deeper breakdown, see our guide to budget categories.

How to Apply the 50/30/20 Rule

To apply the 50/30/20 rule, start by calculating your monthly after-tax income, then multiply by 0.50, 0.30, and 0.20 to find your target spending limits for needs, wants, and savings.

Here’s the five-step version most people can run through in under 30 minutes:

- Calculate your monthly after-tax income — the actual deposit that hits your account, not your gross salary.

- Multiply that number by 0.50, 0.30, and 0.20 to set your monthly targets for needs, wants, and savings.

- List your current expenses and sort each one into needs, wants or savings using the table above.

- Compare your actual totals to the 50/30/20 targets and note where you’re over or under.

- Adjust spending or income until each bucket sits within (or close to) its limit, and repeat next month.

For example: Say you take home $5,000 a month after taxes. Your 50/30/20 targets would be $2,500 for needs, $1,500 for wants, and $1,000 for savings and extra debt payments. If your rent, utilities, groceries, insurance, and minimum debt payments add up to $2,800, you’re $300 over on needs — meaning you may need to trim wants, increase income, or accept a temporary tweak to the percentages.If your fixed costs feel too heavy for the standard split, our deeper look at budget percentages walks through alternatives like 60/20/20 or 70/20/10 that may fit higher cost-of-living areas.

50/30/20 Rule Pros and Cons

The 50/30/20 rule’s biggest advantage is its simplicity — no detailed category tracking required — but it can be too loose for people in debt-payoff mode or anyone whose fixed costs already exceed 50% of income.

Pros

- Simple framework with no detailed category tracking

- Flexible — any spending plan tool can support it

- Easy to remember and easy to teach a partner

- Forces a minimum savings floor, not just a wants ceiling

Cons

- Can be too loose for aggressive debt payoff

- May not work in high cost-of-living areas where rent alone tops 50%

- 20% savings may be too low for late starters or big goals

- Doesn’t account for irregular or freelance income on its own

In short, the 50/30/20 rule is great as a starter framework and as a check on a more detailed budget. If your situation is unusual — heavy debt, variable income, or housing that already exceeds half your paycheck — you may need to adjust the percentages or choose another method.

Best Apps for the 50/30/20 Rule

Rocket Money and Monarch Money are the best apps for the 50/30/20 rule because they automatically categorize your transactions into spending groups, making it easy to see whether you’re staying within each bucket without manual tracking.

Rocket Money

Rocket Money — an all-in-one money app that automatically pulls in your transactions, sorts them into spending categories and flags subscriptions you may have forgotten about.

- What it does: Auto-categorizes transactions into needs, wants and savings buckets.

- Best for: Anyone who wants hands-off tracking and subscription cleanup.

- Pricing: A free tier is available; premium plans typically run $7 to $14 per month.

Monarch Money

Monarch Money — a customizable budgeting app built around shared accounts, custom categories, and goal tracking.

- What it does: Lets you build custom 50/30/20 categories and share visibility with a partner.

- Best for: Couples and detail-oriented budgeters who want to fine-tune the buckets.

- Pricing: Subscription-based, typically around $14.99 per month or $99.99 per year for its Core plan, with a free trial. Get 50% off your first year of the Core Plan with the code MONARCHVIP.

Both apps have paid tiers, so if keeping costs down is a priority, our roundup of the best free budgeting apps includes fully free options as well.

50/30/20 vs. Other Budgeting Methods

The 50/30/20 rule is the most beginner-friendly budgeting method, but zero-based budgeting gives more control for debt payoff, the cash envelope system works better for people who overspend in specific categories, and the pay yourself first method is the simplest option for automating savings.

| Method | Effort Level | Best For | Flexibility | App Support |

| 50/30/20 rule | Low | Beginners and stable incomes | High | Broad (most apps) |

| Zero-based budgeting | High | Debt payoff and detail-oriented planners | Low-Medium | Strong (YNAB, EveryDollar) |

| Cash envelope system | Medium | Habitual overspender in specific categories | Low | Limited (cash-first) |

| Pay yourself first method | low | Automating savings before anything else | High | Broad (any savings/auto-transfer app) |

Want to dig into the alternatives? Compare zero-based budgeting, the cash envelope system and other budgeting methods in one place.

Is the 50/30/20 Rule Right for You?

The 50/30/20 rule is best for beginners, people who find detailed budgeting overwhelming, or anyone with a stable income and manageable fixed costs — it may not work as well if you have high housing costs or significant debt.

It tends to fit well if you’re budgeting for beginners, you have a predictable paycheck and you can reasonably cover your needs with less than half of your take-home pay. The simple split also makes it easier to stick with — there’s less to forget and less to set up.

It can be a struggle if you live in a high cost-of-living city where rent alone exceeds 50% of your income, if your earnings swing month to month, or if any single category is consistently blowing past its target. In those cases, a stricter framework may give you more control.

One specific scenario where the 50/30/20 rule may not be the right fit: anyone carrying high-interest credit card debt — say, balances charging 20% APR or higher — where directing more than 20% of take-home pay to debt payoff is the smart math. The 50/30/20 rule caps the debt-and-savings bucket at 20%, which can slow payoff and let interest charges pile up. If that’s your situation, zero-based budgeting may be a better fit because it lets you assign 30% to 40% of your income to debt while still budgeting for needs and putting a much smaller percentage toward wants. The same logic applies to anyone aggressively chasing a specific savings goal — like a down payment within 12 months — where 20% simply won’t get you there in time.

Frequently Asked Questions

The 50/30/20 rule uses after-tax income — your actual take-home pay, not your gross salary. If you earn $70,000 a year gross but take home about $4,500 a month after taxes and benefits, $4,500 is the number you use as your base.

This is common in high-cost cities. You generally have two options: temporarily adjust the percentages — for example, 60/20/20 — until your housing situation changes, or treat the gap as a signal to increase income or trim other fixed costs. The 50/30/20 rule is a guideline, not a strict rule, and results vary by market.

For many people, 20% is a stretch goal rather than a starting point. Even saving 5% to 10% and automating contributions can build momentum, and a sinking fund or retirement contribution both count toward the 20% bucket.

Minimum debt payments count as needs because you legally owe them. Any extra debt payments above the minimum — like aggressive credit card or student loan paydown — count toward the 20% savings/debt bucket.

The 50/30/20 rule uses broad percentage buckets and skips category-level tracking, while zero-based budgeting assigns every dollar to a specific category before the month begins. The 50/30/20 rule is simpler to maintain; zero-based budgeting gives more control and may suit aggressive debt payoff better.