How to Budget Money: A Beginner’s Step-by-Step Guide

If you’ve ever stared at your bank account at the end of the month and wondered where the money went, you’re not alone. Budgeting is one of those things almost everyone agrees they should do — and that most people put off, try once, get frustrated by, and quietly stop.

Part of the problem is the word itself. “Budget” sounds like restriction — saying no to dinner out, canceling streaming, scrutinizing every coffee. But a real budget isn’t about deprivation. It’s about giving every dollar a job so the money you already earn does more for you.

The good news is that starting a budget doesn’t require an accounting degree, a perfect spreadsheet or a steady paycheck. It takes a few honest numbers, a method that fits your personality and a willingness to adjust as you go. Whether you’re trying to stop living paycheck to paycheck, save for a goal or simply feel less stressed about money, the framework is the same.

How do you actually start a budget when you’ve never made one? Which method works best for beginners? What categories should your money go into, and which apps make tracking easier? We’ll answer all of these questions and more below.

What Is a Budget?

A budget is a plan for how you’ll spend and save your money each month.

At its simplest, a budget is your income minus your expenses, and whatever’s left is assigned a purpose. You start with the money you bring home, subtract everything you need to cover and decide ahead of time what happens to the rest — savings, debt payoff or guilt-free spending.

A good budget is less like a diet and more like a map. It doesn’t tell you what you can’t have; it tells you where your money is already going so you can decide whether you’re happy with it. Most people are surprised by what they find the first time they look honestly.

Quick Comparison: Best Budgeting Apps of 2026

If you’re ready to get started, here’s a quick look at our roundup of the best budgeting apps.

| Budgeting App | Price | Best For | Free Version |

|---|---|---|---|

| Rocket Money | Free; $7–$14/mo for Premium | Subscription tracking, all-in-one | Yes |

| Monarch Money | $14.99/mo; $99.99/yr for Core plan | Couples and full-picture tracking | No (7-day trial) |

| YNAB | $14.99/mo or $109/yr | Zero-based budgeting | No (34-day trial) |

| Cleo | Free; $5.99/mo for Plus | Fun, AI-chatbot engagement | Yes |

| Quicken Simplifi | $6.99.mo, billed annually | Beginners, light users | No (30-day money-back) |

| EveryDollar | Free; $17.99/mo or $79.99/yr for premium | Dave Ramsey followers, Baby Steps users | Yes (requires manual entry) |

| PocketGuard | $12.99/mo for Plus | Knowing what's safe to spend | Yes, but difficult to access |

Why You Should Budget (Even If You Think You Can’t)

A budget gives you control over your money instead of leaving you to wonder where it went.

Most people avoid budgeting because they think it means saying no to everything fun — 48% of Americans simply save what’s left after bills rather than having a plan, according to The Penny Hoarder’s State of Savings survey. But it’s not about a lack of fun. A budget tells you exactly how much you can spend on the things you actually care about because the bills, savings and debt payments are already accounted for.

Budgeting can also reduce the financial stress that quietly eats at a lot of us. The Penny Hoarder’s 2026 Financial Anxiety Barometer found that 43% of Americans worry about their personal finances several times a week — equivalent to 96 days a year. But when you know what’s coming in and going out, the surprise overdraft fees, the credit card statements you’re afraid to open and the late-night anxiety about a car repair start to fade. The money is the same. What changes is how aware of it you are.

There’s also a long-term piece. A budget is what often makes the difference between people who say they want to pay off debt or save for a home and the people who actually do it. Without a plan, money flows toward whatever’s loudest. With a plan, it flows toward what matters to you, even if your situation feels too tight to budget at all.

How to Make a Budget in 5 Steps

To make a budget in five steps, calculate your take-home income, list your monthly expenses, set financial goals, choose a budgeting method, and then track your spending and adjust as you go.

Each step is simpler than it sounds. Most beginners can rough out a first draft of their budget in under an hour.

Step 1: Calculate Your Total Monthly Income

Add up all the money you bring home each month after taxes. Use your take-home pay — the amount that hits your bank account — not your gross salary. Gross income includes money you’ll never see (taxes, health insurance, retirement contributions), and budgeting around it inflates the picture.

Include every source of income, such as:

- Salary or hourly wages, after deductions

- Freelance, side gig or 1099 income

- Tips, commissions or bonuses (use a conservative average)

- Government benefits or child support

- Recurring transfers from a partner or family member

If your income changes month to month, average the past three to six months and use the lower end as your planning number. You can always do more on a bigger month.

Step 2: List All Your Monthly Expenses

Pull the last three months of bank and credit card statements and write down every expense, then split each one into fixed or variable.

Three months is the sweet spot — long enough to catch quarterly bills and irregular charges, short enough to stay manageable. Fixed expenses stay roughly the same each month: rent or mortgage, car payment, insurance, subscriptions and most utilities. Variable expenses fluctuate: groceries, gas, dining out, clothing, gifts and the categories that always seem to surprise you.

For a complete starting list of categories most beginners use, our budget categories guide breaks it down.

Step 3: Set Your Financial Goals

Decide what you want your money to do for you over the next few months and the next few years.

Goals are what make a budget feel worth following. Without them, every “no” feels like a sacrifice instead of a trade-off.

Short-term goals (next 12 months) might include:

- Building a $1,000 starter emergency fund

- Paying off a specific credit card

- Saving for a vacation, a wedding or a car-repair fund

Long-term goals (1–5+ years) might include:

- A fully funded 3- to 6-month emergency fund

- A down payment on a home

- Retirement contributions or kids’ education savings

Write your top one to three goals down. If saving is one of them, our guide on how to save money covers practical ways to free up cash without slashing your quality of life.

Step 4: Choose a Budgeting Method

Pick the budgeting method that fits how you actually live, not the one that sounds most disciplined.

Most beginners pick one of four:

- 50/30/20: 50% of take-home to needs, 30% to wants, 20% to savings and debt. Lowest effort, easiest to start.

- Zero-based: Every dollar of income gets a job until your budget equals zero. Most thorough; requires monthly setup.

- Cash envelope: Withdraw cash for problem categories (dining, groceries, fun) and stop spending when the envelope is empty. Best for visual learners and overspenders.

- Pay yourself first: Move savings and debt payments out of checking the day you get paid; spend the rest. Best if you struggle to save what’s “left over.”

There’s no universally “best” method — just the one you’ll stick with. We compare them in detail in our budgeting methods guide if you want to see them side by side.

Step 5: Track Your Spending and Adjust

Check your spending against your plan at least once a week and adjust the categories that consistently miss the mark.

A budget you set and never look at is just a wish list. The tracking is what turns it into a tool. You have three main options:

- Budgeting app: Connects to your bank, categorizes transactions automatically and shows real-time totals.

- Spreadsheet: More flexibility and zero subscription cost, but you enter transactions yourself.

- Pen and paper: Slowest, but handwriting can boost spending awareness for some people.

Plan to revisit the whole budget once a month — actual versus planned, what worked, what didn’t. The first three months are usually the messiest. By month four, most people land on numbers that hold up. If you’d rather let an app do the heavy lifting, here are a few worth considering.

Popular Budgeting Methods for Beginners

Four popular budgeting methods include 50/30/20, zero-based, cash envelope and pay yourself first — each suited to a different personality and level of effort.

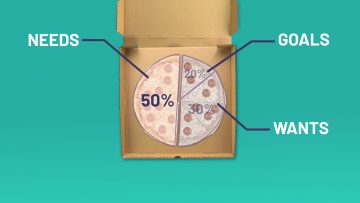

The 50/30/20 Rule

Popularized by Senator Elizabeth Warren in her 2005 book “All Your Worth: The Ultimate Lifetime Money Plan”, the 50/30/20 method splits after-tax income into three buckets: 50% for needs, 30% for wants and 20% for savings and debt repayment. It’s beginner-friendly because it’s forgiving — you don’t have to track every transaction, just keep the three categories roughly in line. Best for: anyone who wants a simple framework without micromanaging.

Zero-Based Budget

A zero-based budget assigns every single dollar of income to a category — savings, rent, groceries, fun, debt — until you’ve allocated income down to zero. Nothing is “leftover” because every dollar already has a job. Best for: people who like detail and don’t mind setting the budget up fresh each month.

Cash Envelope System

The cash envelope system is exactly what it sounds like: you withdraw cash for spending categories that tend to run away from you (groceries, dining out, gas), put each in its own envelope and stop spending in that category when the envelope is empty. The principle works for digital cards too — several apps now offer “envelope” or “vault” features. Best for: visual learners and chronic overspenders.

Pay Yourself First

Pay yourself first flips the order of operations. The day you get paid, you transfer money to savings, retirement and debt before you pay any bills. Whatever’s left funds your normal spending. Best for: anyone who finds that “saving what’s left at the end of the month” leaves nothing to save.

Compare Methods

| Method | Best For | Time Required | Flexibility | Tracking Style |

|---|---|---|---|---|

50/30/20 Rule |

Beginners who want simplicity |

Low |

High |

Three-bucket totals |

Zero-Based Budget |

Detail-oriented planners |

High (monthly setup) |

Medium |

Every dollar tracked |

Cash Envelope |

Overspenders who need limits |

Medium |

Low–Medium |

Cash or app envelopes |

Pay Yourself First |

Savers who can’t save at month’s end |

Low |

High |

Auto-transfers |

There’s no universally “right” answer here. The method you’ll stick with for six months will outperform the one that sounds best on paper.

Best Budgeting Apps for Beginners

The best budgeting app for a beginner is the one you’ll actually open — usually one with automatic bank syncing, plain-English categories and an interface that doesn’t feel like accounting software.

A few things to look for: secure bank connections, support for the budgeting method you plan to use (some apps are built for zero-based, others for cash flow), pricing that fits your situation and a mobile app that’s pleasant to use day to day. Free apps are great until they aren’t — most paid apps charge $5 to $15 per month, which can pay for itself if it stops one impulse buy.

Rocket Money

Rocket Money is a budgeting and bill-management app that flags forgotten subscriptions and can negotiate recurring bills on your behalf.

- Typical pricing: Free basic version; Premium uses a “pay what you think is fair” model from $7–$14 per month

- Mobile + web: Yes

- Best for: Beginners who want a basic budget plus subscription cleanup

Pros:

- Free version covers most budgeting basics

- Subscription scanner finds bills you forgot about

Cons:

- Unlimited custom categories and savings goals are paywalled in Premium

- Bill negotiation takes a percentage of any savings

Monarch Money

Monarch Money is a paid budgeting app focused on couples and families, with collaborative budgeting and detailed net-worth tracking.

- Typical pricing: $14.99 per month or about $99.99 per year for Core plan, $199.99 a year for Plus. Get 50% off your first year of the Core Plan with the code MONARCHVIP.

- Mobile + web: Yes

- Best for: Couples or anyone who wants a clean, customizable interface

Pros:

- Built for sharing — invite a partner at no extra cost

- Investments, real estate and crypto track in one place

Cons:

- No free tier

- Slightly steeper learning curve than Rocket Money

YNAB

YNAB (You Need A Budget) is the most thorough zero-based budgeting app on the market, built around the philosophy of giving every dollar a job.

- Typical pricing: $14.99 per month or $109 per year, with a 34-day free trial

- Mobile + web: Yes

- Best for: People who want to be more intentional and don’t mind a learning curve

Pros:

- Strong educational content and free workshops

- Highly customizable categories and goals

Cons:

- Steepest learning curve of the apps listed

- More hands-on than passive trackers

Offers change; verify terms.

Cleo

Cleo is an AI-powered budgeting assistant with a chat interface — it answers questions about your spending in conversational style and (if you ask it to) will roast your spending habits.

- Typical pricing: Free basic version; Cleo Plus is $5.99 per month, Cleo Pro is $8.99 per month and Cleo Builder is $14.99 per month.

- Mobile only

- Best for: Younger budgeters who want a casual, gamified feel

Pros:

- Free version is genuinely useful

- Friendly tone makes daily check-ins less intimidating

Cons:

- Cash advances and credit-building features sit behind paid tiers

- Less detail than Monarch or YNAB

Offers change; verify terms.

For a fuller side-by-side, see our roundup of the best budgeting apps.

How to Budget by Category

A common starting framework is the 50/30/20 rule, which splits after-tax income into 50% for needs, 30% for wants and 20% for savings or debt repayment.

Most beginners ask the same question: how much should I spend on X? There isn’t a universal answer — costs vary wildly by city, family size and life stage — but the table below shows reasonable starting ranges for each major category, using a $4,000-per-month take-home income as an example.

Quick comparison

| Category | Range | Sample | Notes |

|---|---|---|---|

Housing |

25–35% |

$1,000–$1,400 |

Often higher in HCOL cities; aim under 30% |

Food |

10–15% |

$400–$500 |

Includes groceries plus modest dining out |

Transportation |

10–15% |

$400–$500 |

Drops sharply if no car payment, walkable cities |

Savings & Emergency Fund |

10–20% |

$400–$600 |

Build $1,000 starter fund first, then 3–6 months |

Debt Repayment |

5–15% |

$200–$400 |

Higher if paying down credit cards aggressively |

Health care |

5–10% |

$200–$300 |

May be partly pre-tax via employer; build a buffer |

Personal and entertainment |

5–10% |

$200–$300 |

Streaming, hobbies, gifts |

Percentages are guidelines, not rules — adjust based on your income, location and goals.

Here’s how each category typically breaks down:

Housing: rent or mortgage, property tax, HOA, renters or homeowners insurance and basic utilities. The rule of thumb is 25–35% of take-home, but in high-cost cities, that can stretch.

Food: groceries and essential household items, plus a small dining-out allowance for most beginners. If your grocery line keeps blowing past target, planning meals two weeks at a time and shopping with a list can pull it back without much pain.

Transportation: car payment, gas, insurance, maintenance, parking or transit costs. If gas is a major line item, a cash-back app like Upside (a cash-back app for gas, groceries and restaurants — not a budgeting app) may offset some of the cost.

Savings & Emergency Fund: emergency fund contributions and short-term savings. Many beginners aim for at least $1,000 in a starter emergency fund first, then build toward 3–6 months of expenses over time.

Debt Repayment: minimum payments on credit cards and loans, plus any extra you can put toward principal. If your minimums are eating most of this category, you may need to look at the bigger picture (more on that in the next section).

Health care: insurance premiums (if not deducted pre-tax), copays, prescriptions and out-of-pocket costs. Easy to underestimate; build in a buffer.

Personal & Entertainment: streaming, hobbies, subscriptions, gifts, dining out and the everyday “wants” that make life feel like more than just bills.

Budgeting Tips for Beginners

The strongest beginner budgeting tips focus on building habits, not slashing costs.

A few of the highest-leverage moves:

- Automate savings the day you get paid. If saving comes after spending, there’s usually nothing left to save.

- Start a sinking fund for predictable irregular expenses — car maintenance, holiday gifts, annual insurance premiums. A few dollars set aside each month prevents a $400 surprise from blowing the whole budget.

- Use cash for problem categories. If groceries or dining out is the leak, the friction of physical cash creates a natural ceiling.

- Schedule a weekly money check-in. Fifteen minutes once a week is enough to see what’s tracking and catch problems before they grow.

- Keep one fun category. Budgets that allow zero discretionary spending tend to fail within weeks. Build in a small allowance for the things you actually enjoy.

- Review monthly, adjust quarterly. Your budget should evolve as your life does.

- Don’t aim for a perfect month. Aim for a slightly better one than the last.

For some readers, a personal loan to consolidate high-interest debt may lower monthly payments and make budgeting easier — marketplaces like MoneyLion offer rate comparison tools, and results vary based on credit.

For those with substantial debt that feels unmanageable who also feel like they’ve run out of options, working with a debt settlement program (such as National Debt Relief or Freedom Debt Relief) may be a starting point.

Frequently Asked Questions

The 50/30/20 rule is a budgeting framework that splits your after-tax income into three buckets: 50% for needs, 30% for wants and 20% for savings and debt repayment. The percentages are flexible — many beginners adjust them based on cost of living and goals.

The best budgeting method for beginners is usually the 50/30/20 rule because it’s the simplest to start, but the right method depends on personality. People who like structure often prefer zero-based budgeting, while overspenders may have more success with cash envelopes. The “best” method is the one you’ll stick with for at least three months.

Budgeting on a low income starts with the same five steps as any budget, with two adjustments: prioritize essentials before anything else, and treat increasing income as a budget line, not just cutting expenses. Building even a $500 starter emergency fund can prevent one surprise bill from undoing months of progress.

It depends on your habits. A budgeting app is faster, syncs automatically and works well for people who don’t enjoy data entry. A spreadsheet is free, infinitely customizable and works well for people who want full control over the categories and formulas. Many beginners start with an app and graduate to a spreadsheet — or vice versa — as they figure out what they actually want to see.

Sticking to a budget is mostly about reducing friction and reviewing often. Automate savings and bill payments so you can’t forget them, do a 15-minute weekly check-in and rebuild realistic categories each month rather than punishing yourself for missing the last one. Most budgets fail not because of weak discipline but because the numbers were unrealistic to begin with.

A sinking fund is a category where you save a small amount each month toward a known irregular expense — car maintenance, holiday gifts, an annual insurance premium or a future vacation. Instead of getting blindsided by a $400 car repair, you’ve already set the money aside. Sinking funds are one of the simplest ways to make a budget feel less fragile.