YNAB Review 2026: Is You Need a Budget Worth $14.99 a Month?

If you’ve ever sat down to write out a budget, felt great about it for two weeks and then watched the whole thing fall apart by month’s end, you’re far from alone. The hardest part of budgeting isn’t the math, it’s the system. Without a structure that tells you what to do when life gets messy, even the most organized spreadsheet eventually collapses.

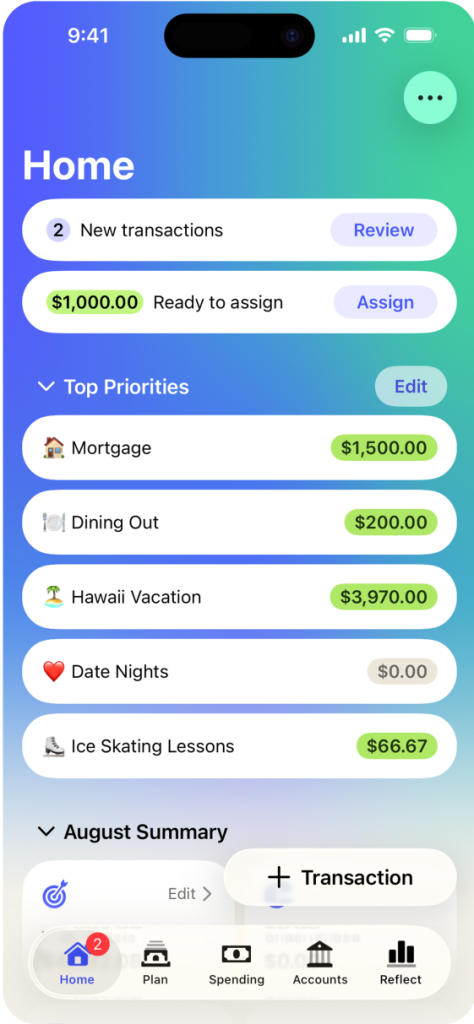

YNAB, short for You Need a Budget, is a personal finance app built around a specific structure called zero-based budgeting. Instead of tracking what you’ve already spent, YNAB asks you to assign every dollar a job before it leaves your account. The system has earned a devoted following: paycheck-to-paycheck breakers, debt payoff warriors and people who simply want to feel in control of their money.

But YNAB isn’t free, and at $14.99 a month or $109 a year, it’s one of the more expensive budgeting apps on the market, especially in 2026, when several free competitors have either shut down (Mint) or pivoted (Empower, formerly Personal Capital). For a paid app to be worth it, it has to deliver more than what the free options provide.

So is You Need a Budget worth the cost? We’ll answer all of these questions and more below.

What Is YNAB?

YNAB (You Need a Budget) is a personal finance app built around zero-based budgeting, a system in which you assign every dollar of income to a specific purpose before you spend it.

Founded in 2004, YNAB has grown from a desktop spreadsheet into a subscription-based app available on iOS, Android, the web and Apple Watch. Unlike many of its competitors, YNAB does not sell user data, run ads or earn affiliate fees from partner banks. Its only revenue source is the subscription itself.

YNAB doesn’t have a permanent free tier. After a generous trial period, users either subscribe or lose access. That structure makes it different from “freemium” apps like Rocket Money or Monarch Money, where free versions are limited but functional. With YNAB, you’re paying for the methodology as much as the software — the company offers extensive workshops, written guides and customer support designed to teach the philosophy behind its system.

For readers brand-new to the basics, our budgeting for beginners guide is a useful starting point before deciding if YNAB’s deeper system is the right fit.

YNAB costs $14.99 per month or $109 per year, with a 34-day free trial.

The annual plan saves about $70 a year compared with paying monthly, roughly $9.08 a month if you spread the annual cost. Either tier comes with the same full feature set; YNAB does not have premium tiers or paywalled features beyond the standard subscription.

A few additional pricing details to know:

- Student discount: Full-time college students with a valid .edu email can get YNAB for $4.99 a month for one year, or in some cases free for 365 days through YNAB’s College Program.

- Family sharing: A single subscription covers up to six people who can share the same budget. There is no extra charge per additional user.

- 34-day free trial: The longest free trial of any major budgeting app, with no credit card required.

How YNAB Works: The Four Rules

YNAB is built around four guiding principles it calls its rules — a system for taking control of your money before you spend it.

The four rules are what make YNAB feel different from other budgeting apps. They’re not a rigid spreadsheet; they’re a framework for making decisions when reality doesn’t match your plan.

Rule 1: Give Every Dollar a Job

Assign every dollar of income to a category before you spend it.

Whenever you get paid, you allocate that money to specific categories — rent, groceries, savings, debt payoff, entertainment — until your unassigned balance hits zero. The math is simple: Income minus assignments should equal $0. The discipline is harder, but it forces you to confront where your money should go before life chooses for you.

Rule 2: Embrace Your True Expenses

Plan for irregular expenses by setting money aside monthly, so they don’t blow up your budget when they arrive.

Car repairs, holiday gifts, insurance premiums and back-to-school costs aren’t surprises, they’re predictable expenses that happen at irregular intervals. This rule turns them into monthly line items so you’re never caught off guard. By the time the bill arrives, the money is already there.

Rule 3: Roll With the Punches

When you overspend in one category, move money from another instead of declaring the budget broken.

YNAB is explicitly designed to flex when life happens. Spent more on groceries this week? Move money from your dining-out category and keep going. There’s no shame system or penalty, just a quick adjustment that keeps the larger plan intact.

Rule 4: Age Your Money

Aim to spend money that is at least 30 days old, so today’s bills are paid with last month’s income, not last week’s.

The longer your money ages before you spend it, the further you’ve moved from living paycheck to paycheck. The goal is to build a buffer where today’s deposits aren’t immediately needed for today’s expenses. For readers struggling with this cycle, our guide on living paycheck to paycheck covers complementary strategies.

YNAB Features

YNAB’s main features include bank syncing, goal tracking, detailed reports, family sharing and a full mobile experience.

Bank Sync and Direct Import

You can connect bank accounts directly through YNAB’s secure import system, which pulls in transactions automatically. For accounts that don’t sync, manual entry or file import is supported. Most users prefer the automatic approach, but some intentionally enter transactions by hand to feel more connected to each purchase.

YNAB supports most major U.S. and Canadian banks. When direct sync isn’t available, you can upload an OFX, QFX or CSV file from your bank to keep transactions current.

Goal Tracking

YNAB lets you set savings goals (emergency fund, down payment), debt payoff targets (credit cards, student loans) and monthly funding goals (bills, subscriptions). The app shows progress visually as you fund each category, which is especially motivating for debt payoff goals where momentum matters.

Goals can be one-time targets, monthly funding amounts or weekly contributions, and YNAB will tell you how much you still need to assign each month to stay on track. For users tackling multiple debts, the per-category targets pair well with strategies like the debt snowball or avalanche.

Reports

The reports section includes spending by category, net worth over time and income vs. expense charts. Reports become most useful after a few months of consistent data, when patterns start to emerge. Many longtime users say the reports are where the real “aha” moments happen — discovering, for example, that they’ve been spending more on takeout than on groceries or that their utility costs spike predictably every winter. Filters let you compare time periods, drill into a single category, or look at totals across multiple accounts.

YNAB Together (Family Sharing)

A single YNAB subscription supports up to six people who can share the same budget. This is unusually generous compared to other budgeting apps and is a common reason couples and families choose YNAB. Each person logs in with their own account but contributes to the same shared plan.

Mobile Apps

YNAB has full-featured iOS and Android apps, a web app for desktop use and an Apple Watch companion. Most users move between devices throughout the month — entering transactions on mobile, doing deeper budgeting on desktop and checking goal progress at a glance on the watch. Data syncs in real time across devices, so a transaction entered at the grocery store shows up on the desktop dashboard immediately.

How Long Is the YNAB Free Trial?

YNAB offers a 34-day free trial, the longest free trial of any major budgeting app, with no credit card required.

During the trial, you get full access to every feature: account syncing, all four rules in action, family sharing, the reports section and mobile apps. There are no paywalled features, no nagging upgrade prompts and no automatic billing if you forget to cancel, because no card was required to start.

YNAB also offers a free year for verified college students through its college program.

Is YNAB Worth It?

YNAB can pay for itself if you save even $10 a month thanks to the system, but it requires active engagement to deliver value.

The math is straightforward: at $109 a year, breaking even means saving roughly $9 a month, a low bar if the methodology helps you cut even one or two unnecessary expenses. YNAB reports that new users save an average of $600 in their first two months and more than $6,000 in their first year. Results vary, though, and these numbers reflect users actively engaged with the system.

YNAB is best suited for hands-on budgeters: people who want to be involved with each dollar, who are working on debt payoff or who are trying to break the paycheck-to-paycheck cycle. It is less ideal for passive money managers who want spending awareness without active participation, or for users whose primary need is investment tracking. For passive insights, Monarch Money tends to be a better match. For more general guidance on saving, see our how to save money guide.

If unmanageable debt is part of the picture, a paid app alone may not be enough. Debt-relief programs from companies like National Debt Relief or Freedom Debt Relief may help readers with significant unsecured debt explore options like consolidation or settlement, though terms and eligibility vary.

YNAB Pros and Cons

YNAB’s biggest strengths are its zero-based methodology and family sharing; its biggest weaknesses are the lack of a free tier and the learning curve required to get value. Here’s a look at its pros and cons:

Pros

- Powerful zero-based system with the four rules framework

- 34-day free trial, no credit card required

- Family sharing for up to six people at no extra cost

- Student discount available

- Web, mobile and Apple Watch apps

- Active community and live workshops

- No ads, no data selling

Cons

- Steep learning curve in the first month

- Requires active engagement — passive use won’t deliver value

- No native investment tracking

- No bill negotiation feature

- More expensive than free alternatives like Empower (formerly Personal Capital)

- Bank sync occasionally needs manual reconnection

Who Should Use YNAB?

YNAB is built for hands-on budgeters who want full control over every dollar, not for passive users who simply want awareness of their spending.

YNAB tends to be a strong fit for:

- People paying down credit card or student loan debt

- Households trying to break the paycheck-to-paycheck cycle

- Couples or families with up to six members sharing finances

- Students with a .edu email seeking the discount

- Anyone who has tried free budget apps and bounced off

It tends to be less of a fit for:

- Passive users who want autopilot insights, Monarch Money is a better choice

- Users focused mainly on canceling subscriptions, Rocket Money handles that more directly

- Investment-focused users who want brokerage tracking

- Anyone unwilling to spend 30 minutes a week maintaining the budget

For broader options, our best budgeting apps roundup covers paid and free choices side by side, and the EveryDollar review goes deeper on a popular alternative zero-based system.

YNAB vs. Monarch Money vs. Rocket Money

YNAB excels at strict zero-based budgeting, Monarch Money excels at full-picture financial tracking and Rocket Money excels at managing subscriptions. Here’s a look at YNAB vs. its biggest competitors:

YNAB vs. Monarch Money vs. Rocket Money

| Feature | YNAB | Monarch Money | Rocket Money |

|---|---|---|---|

Price |

$14.99/month or $109/year |

$14.99/month or $99.99/year for its Core plan |

$7–$14/mo (pay-what-you-want) |

Free Tier |

None (after trial) |

None (after trial) |

Yes |

Trial Length |

34 days |

7 days |

7 days |

Budgeting Style |

Zero-based |

Customizable |

Category + automated, bills |

Best For |

Hands-on budgeters |

Couples, full tracking |

Subscriptions, bills |

Unique Feature |

Four rules methodology |

Investment + net worth |

Bill negotiation |

Choose YNAB for strict zero-based budgeting and debt payoff. Choose Monarch for a fuller financial picture, including investments. Choose Rocket Money to track and cancel subscriptions or negotiate recurring bills. For deeper looks, see our Monarch Money review and Rocket Money review.

Final Verdict

YNAB is one of the most effective budgeting tools available, but only for the right kind of user. Its zero-based system and four rules framework consistently help engaged users save money, pay off debt and break the paycheck-to-paycheck cycle. The 34-day trial gives you a fair window to test whether the methodology clicks before you spend a dollar.

The price is the obstacle. At $14.99 a month or $109 a year, YNAB is among the more expensive budgeting apps in 2026, especially compared with Empower (formerly Personal Capital) and other free alternatives that emerged after Mint shut down. The student discount and family-sharing-for-six help close the gap for the right households.

If you’re willing to spend a few hours a week reviewing your money and making active decisions, YNAB can deliver real, measurable results. If you want autopilot, this isn’t your app. But if you’re reading this review because more passive tools haven’t worked, that may actually be the strongest argument for trying the 34-day free trial. Test it for a full pay cycle before deciding whether the subscription fits into your budget.

YNAB FAQs

No. YNAB does not offer a permanent free tier. New users get a 34-day free trial with no credit card required, and verified college students may qualify for a free year through the YNAB college program. After that, the subscription is required to continue.

YNAB is $14.99 per month, or $109 per year (about $9.08 per month if you pay annually). Students with a valid .edu email may get $4.99 per month for one year.

For hands-on budgeters working on debt payoff or trying to break the paycheck-to-paycheck cycle, YNAB can pay for itself many times over. For passive users who only want occasional spending awareness, free alternatives may be a better fit. Results vary.

Yes. Verified college students with a .edu email can get YNAB for $4.99 a month for one year, and YNAB’s college program offers a free year to eligible students.

The four rules are: Give Every Dollar a Job, Embrace Your True Expenses, Roll With the Punches and Age Your Money. Together they form a complete framework for taking control of money before it gets spent rather than after.

Yes. A single YNAB subscription covers up to six people and is one of the most popular tools for couples managing money together. Both partners can log in with their own accounts and contribute to a shared budget without any additional cost.