This SAHM of 4 Reveals Her Exact Budget for Living Richly on $36,000 a Year

Here at The Penny Hoarder, we do our best to both inform and inspire our readers.

But oftentimes, it’s you who inspire us.

Such is the case with Melissa Palmer, a Penny Hoarder reader who left this comment on one of our Facebook posts:

We raise three kids (with a fourth on the way) on my husband’s $36,000 a year salary. We sacrifice a lot, but yet we never feel poor. And all the things we ‘sacrifice,’ we don’t actually care about… We feel so very, very rich and blessed. We are not lucky. We CHOSE this. And I believe most families can as well, but choose not to.

Intrigued and impressed, we had to know more. So we asked her to share her story.

Melissa’s situation won’t apply to everyone. She and her husband, for example, made a smart real estate investment early on, and pay less rent by living on his parents’ property, which isn’t possible for everyone.

If you can't pay rent, here's how to negotiate with your landlord.

But no matter who you are, we’re confident her budgeting tips and frugal outlook will help and inspire you.

Take it away, Melissa!

Thanks so much for chatting with us. To start, can you walk us through your financial history up until now?

Several years ago in Tucson, we bought a house off Auction.com for $53,000. It was an absolute miracle.

The house was completely livable, and with our two incomes at the time (we made about $50,000, which now I can’t believe we made that much!), we got through the mortgage, flipped the house and sold it three years later for $134,000.

We got a big fat check for a little over $68,000, so we paid off our $25,000 in student debt and moved to Spokane with our two kids, into a 1,200 square-foot apartment on Cole’s parents’ property (where we currently live).

We’ve been in this apartment for almost two years, and last August, we used another chunk of change from the house flip to purchase five acres nearby for $25,000. We’re in the process of preparing the land and purchasing a new 1,800 square-foot manufactured home to put on it.

Great. Can you break down your budget in detail?

Cole works full time as a delivery driver and chimney sweep. Our income is about $2,800 per month (full time at $18 per hour, plus time-and-a-half overtime pay).

Here are our monthly expenses:

Car insurance: $137 (for two cars)

Gas: $150

Rent: $500

Cell phones: Under $30 with Republic Wireless (as low as $26, depending on how much data we use)

Groceries: $480 (includes household items like dog food, diapers, soap, etc)

Restaurants: $60 (date night)

Additional food: $60 (snacks, coffees, takeout pizza)

Church tithes: $280

Extra giving: $50

Everything else: $500

Savings: $550

(Author’s note: Since Melissa’s husband doesn’t receive benefits at his job, their family qualifies for state health insurance.)

Anything else we should know about your budget? How will things change when you move?

With our tax refund, we tithe 10%, pay our life insurance for the year (about $500) and save the rest.

Once we have our own house and property, our mortgage will be about $120,000, which means our payment will be about $800-$900 each month. We’ll then also use our tax return to pay our power bill for the year (we’ll have well [water] and septic, so no monthly bills there).

We won’t be able to save very much then — besides our tax refund — but we’re OK with that. Even after moving to our property, we’ll keep $7,000 in savings as an emergency fund.

How do you track your spending? How has it made a difference?

I record every single purchase; every penny is accounted for. I just use an Excel spreadsheet and keep receipts for the month.

[Author’s note: You can also use Google Sheets like this family, or a free budgeting app like Mint.]

Every day, I take 30 seconds and type in what we spent that day. Super easy, and eye-opening at the end of the month to see what we spent money on.

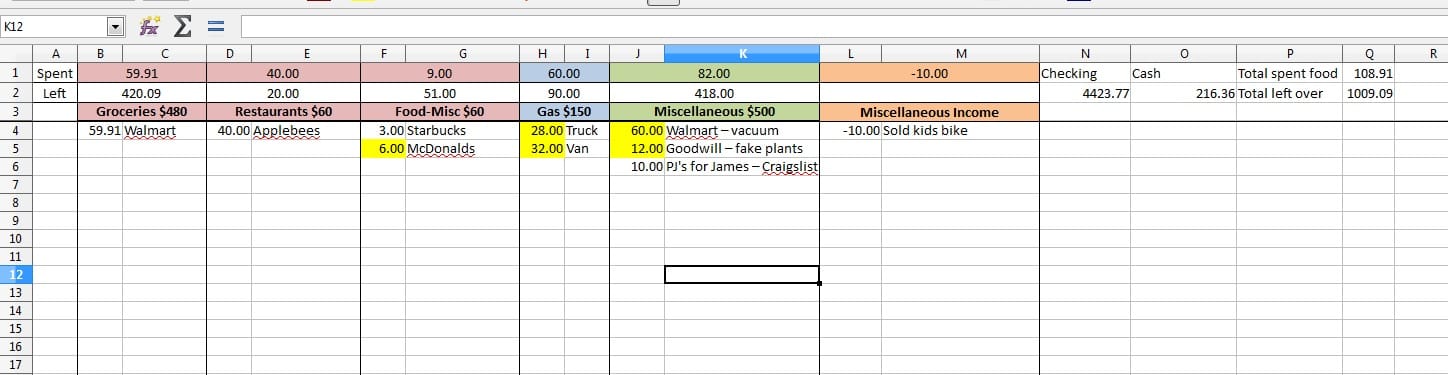

Each month, I make a new tab in the spreadsheet to keep track of that month’s expenses. Highlighted numbers are debit/credit transactions, and white numbers are cash (so I can reconcile it at the end of the month).

To the right, the numbers under “Checking” and “Cash” are the starting balances for that month, and at the end of the month, I’ll put the ending balances after reconciling underneath them. I keep receipts — so that at the end of the month, if numbers don’t match up, I can go back and see what I missed.

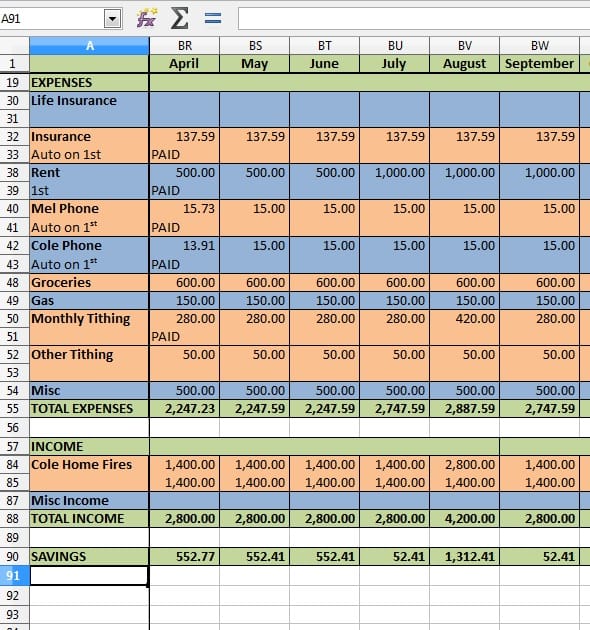

Then I put these numbers into our “big picture” finances tab, which looks like this:

The actual amounts spent on groceries, gas, etc, are put in at the end of the month to see how we did and what our savings are for that month. I then gray out that column and move on to the next month! If I scroll to the left, you’d see all the previous months.

I started this in January 2015, and it has made a huge difference for us, allowing us to see exactly what we are spending our money on.

And when you need to RECORD and be held ACCOUNTABLE for each penny spent, we’ve found you spend it more carefully.

Can you share some of your budgeting tips and strategies?

We rarely buy things we don’t need, and I buy almost everything secondhand, from clothes to toys and home decor, etc.

I also sell stuff on Craigslist and look for restaurant coupons before date nights.

Get Cash Back

I use our cash-back credit card for almost all purchases.

I never keep a balance on it — I just use it for the cash back. I pay it off immediately after spending the money.

Use Savings Catcher

I do almost all of my grocery and household shopping (except produce, [which is] cheaper at Winco) at Walmart, so I use the Savings Catcher app.

All you have to do is scan the code at the bottom of each receipt — and if the app finds out there are cheaper deals at other stores for things you purchased, it gives you the difference (which you can get as a Walmart gift card).

Download Media Insiders

I have Media Insiders on my phone and PC, which just runs in the background and logs which TV shows and movies I watch.

Again, it’s not much, but this one earns about $50 every three months. It’s just a “set it and forget it” thing, and every few months I’ll pull out enough for a nice little date night for Cole and me.

Cook at Home

I think this is one of the biggest savings. I find if I do at least a weekly menu, based on what produce was on sale, it’s less stressful and I don’t waste as much.

We buy our meat from GoDirect Foods, which has super cheap and high-quality meats.

Start a Side Business

I also have a VERY small side business at home where I make bow ties for little baby boys. I give more away as gifts than I actually sell, but it’s still fun for me.

Those are awesome tips! How do you maintain such a frugal perspective?

One summer when we lived in Tucson, Cole worked for $10 an hour splitting firewood… outside in the 110-degree summer heat. It was absolutely dreadful work for him.

When I would pass a Starbucks and want to stop and get a latte, I’d think, “That’s half an hour of Cole splitting firewood outside.”

Since then, I’ll consider “unnecessary” purchases through either the lens of how much work Cole is doing for that item, or how it compares to a “necessity” item like milk (this item costs two gallons of milk — is it worth it?).

I’m not saying we never splurge on unnecessary items, but shifting your perspective to look at the time and energy required to purchase the item, or what other items you could purchase instead, helps you realize what you really need.

You said you “never feel poor.” How do you enrich your life on a limited budget?

Really, I think it comes down to simply living within your means. Analyzing what your family actually NEEDS versus WANTS, and shifting your perspective accordingly.

If I felt like I needed a huge 2,000 square-foot home, then I’d always feel discontent in a smaller home. I think realizing how much you really have causes you to be grateful and content.

Also, I’ve found the more generous you are, the more God blesses you.

Even if you consider yourself to have a “little” or to be “in need,” you still have more than enough to give to those who are in greater need. Even small gestures — like picking up a cup of coffee for a mom you know is having a hard day — go a long way, and make life so much fuller.

Our life is very rich, and very full.

We make quality family time a priority, and we almost always have family dinners together (at our dining table, not in front of the TV).

Cole and I make time for each other with date nights (exchanging babysitting with other couples with kids), as well as time in the evening together after the kids are in bed.

Really, I think living a simpler life (with fewer expectations of what life “owes” you, or what you need to have to enjoy life) leads to a more joy-filled and enriched life.

What would you say to someone who wants to stay home, but doesn’t think they can do so financially?

Honestly, I would ask, “Are you willing to change your lifestyle to stay home?” If so, then you probably can.

If your current lifestyle doesn’t work financially for you to stay home, then downsize.

Sell the house and buy a cheaper house. Sell the cars and buy cheaper cars. Cut out monthly bills where possible. Don’t spend money you don’t have. Sell stuff (you probably have a lot of stuff you don’t use or need anyways).

If drastic measures need to be taken — like you live in a super expensive city and would need to move either to the outskirts, or quite a bit further — if you’re really serious, then do it.

Trust me, it’s worth it. What you gain far outweighs what you “sacrifice.”

What’s one misconception of stay-at-home parents you’d like to clear up?

That it’s by “luck” or “chance” or because “your husband must make a lot of money” that I GET to stay home. Not at all true.

It’s a huge decision every parenting couple (because obviously single parents aren’t in the same boat) makes.

Whichever way they choose — to live off one income or two — they’re indeed CHOOSING it. It’s not a decision they’re forced into, one way or another.

Are you happy with your decision to stay home? Do you have any regrets?

I wouldn’t change anything. I can’t imagine I’ll look back at the end of my life and wish I would’ve been at work instead of raising our children.

I really don’t feel like we’ve sacrificed anything — at least not anything we really cared about.

The only “plus” to not staying at home would be more money, and I’m not convinced at all that more money equals more happiness.

We don’t feel like we’re simply “surviving”; we really do feel so very rich and blessed with our life.

Susan Shain, senior writer for The Penny Hoarder, is always seeking adventure on a budget. Visit her blog at susanshain.com, or say hi on Twitter @susan_shain.